Above Photo: Jessie Suren borrowed about $71,000, most of it from Sallie Mae, to attend La Salle University in Philadelphia. But a job with the U.S. Marshals Service fell through, and by her 2010 graduation, she had a soaring loan balance and no career prospects.Credit: Peter van Agtmael/Magnum Photos

42 million people owe in student debt.

It’s a profit center for Wall Street and the government. Here’s how we got into this mess.

A generation ago, Congress privatized a student loan program intended to give more Americans access to higher education.

In its place, lawmakers created another profit center for Wall Street and a system of college finance that has fed the nation’s cycle of inequality. Step by step, Congress has enacted one law after another to make student debt the worst kind of debt for Americans – and the best kind for banks and debt collectors.

Today, just about everyone involved in the student loan industry makes money off students – the banks, private investors, even the federal government.

Jessie Suren is an energetic 28-year-old who wanted a career in law enforcement. Albert Lord is a 70-year-old former accountant who became a multimillionaire executive. The two have never met, but their stories tell the history of America’s student debt crisis.

Suren attended a free boarding school for underprivileged youth in Hershey, Pennsylvania, and enrolled in La Salle University in Philadelphia. Scholarships didn’t cover the cost of the private college, so she borrowed about $71,000, much of it from Sallie Mae, the financial giant of the student loan industry.

Suren did well in school. But a job with the U.S. Marshals Service fell through, and by graduation in 2010, she had a soaring loan balance and no career prospects.

In the years since then, Suren has scrambled to keep current on her loans, sometimes working 16 hours a day at two low-paying jobs. Her finances are incredibly tight, and she has made no headway on her loans. Today, her balance tops $90,000.

“My loans are a black cloud hanging over me,” she said. “I’m a student debt slave.”

For Lord, student loans have been the road to riches. He was the CEO who built Sallie Mae into a financial colossus through fees, interest and commissions on billions of dollars of federally guaranteed student loans. For delivering handsome profits to investors, Lord received pay and stock worth hundreds of millions of dollars.

His success made him one of the highest-paid executives in Washington, gave him entrée into an elite circle of power brokers and won him a seat on the board of the Washington Redskins Charitable Foundation. With his wealth, he started a private equity company and built his own golf course, Anne Arundell Mannor, near the Chesapeake Bay. After a 30-year career at the forefront of the student loan industry, Lord retired in 2013 and now shuttles between houses in Naples, Florida, and Annapolis, Maryland.

Almost every American knows someone like Suren, an adult burdened by a student loan. Fewer know that growing alongside the legions of indebted students is a formidable private industry that has been enriched by student debt.

Decades ago, the federal government relinquished direct control of the student loan program, opening its bank to corporations concerned with profits, not diplomas. Private equity companies and Wall Street banks seized on the flow of federal loan dollars by peddling loans that students sometimes could not afford and then collecting fees from the government to hound those students when they defaulted.

Once in place, the privatized student loan industry has succeeded largely in preserving its status in Washington. Student loans are virtually the only consumer debt that cannot be discharged in bankruptcy except in the rarest of cases – one of the industry’s greatest lobbying triumphs.

At the same time, societal changes conspired to drive up the basic need for these loans: Middle-class incomes stagnated, college costs soared and states retreated from their historical investment in public universities.

If states had continued to support public higher education at the rate they had in 1980, they would have invested at least an additional $500 billion in their university systems, according to an analysis by Reveal from The Center for Investigative Reporting.

That’s an amount roughly equal to the outstanding student debt now held by those who enrolled in public colleges and universities.

The calculus for students and their families changed drastically, with little notice. Today, there is a student debt class like no other: more than 40 million Americans bearing $1.3 trillion in debt that’s altering lives, relationships and even retirement.

One of the winners in the profit spree behind this debt: the federal government. By the Department of Education’s own calculations, the government earns in some years an astounding 20 percent on each loan.

“The United States government turns young people who are trying to get an education into profit centers to bring in more revenue for the federal government,” Sen. Elizabeth Warren, D-Mass., said on the Senate floor in February. “This is obscene. The federal government should be helping students get an education – not making a profit off their backs.”

The student debt crisis is a microcosm of America – a tale of the haves and have-nots. Students who attend the richest schools often have less debt than students who graduate from state colleges. Students from low- or moderate-income families who attend for-profit schools usually take on the heaviest debt load of all.

The imbalance between those with debt and those without will exacerbate income inequality for decades to come.

The Obama administration has taken steps toward reform. It has eliminated the financial middlemen who long collected a fee to issue federal loans. The government now loans directly to students, though private companies continue to administer the loans. New regulations limit student debtors’ federal loan payments to 10 percent of their income.

But the basic system remains in place: Contractors with historically little oversight from the federal government have an incentive to make a profit by collecting as much as they can from student debtors.

Today, student debt is a $140 billion-a-year industry. And unlike many of its customers, the industry’s future looks bright.

Strolling through a rally of New York University students protesting rising loan debt, a writer for a debt industry publication found himself face to face with students carrying placards and wearing T-shirts proclaiming their frustration. But all he could see were dollar signs.

“I couldn’t believe the accumulated wealth they represented – for our industry,” he wrote in insideARM. “It was lip-smacking. … We are in for lifetime employment!”

The NYU rally was in 2011. In the five years since, total debt has risen by nearly half a trillion dollars.

The privatization of a system meant to cure inequality

It’s not hard to see why people such as Jessie Suren are feeling squeezed and misled – and why loans that appeared smart and easy turned out to be anything but.

Stories such as Suren’s are everywhere, whether the borrowers attended prestigious universities or for-profit colleges, whether they wanted to be computer programmers or fashion designers, whether they were studying biology or graphic design.

Members of the new debtor class talk about how easy it was to borrow to go to college and how no one, not even their parents, warned them about the risk they were assuming. They talk about colleges that made it seem safe to borrow by assuring them that everyone had loans. They talk about how they want to pay off their loans but can’t earn enough to do that.

They say they didn’t realize how dramatically their loan balance could soar if they missed payments. They speak of the embarrassment of being hounded by debt collectors. And they talk about the stress – the unrelenting stress – of knowing they probably never will be free of debt.

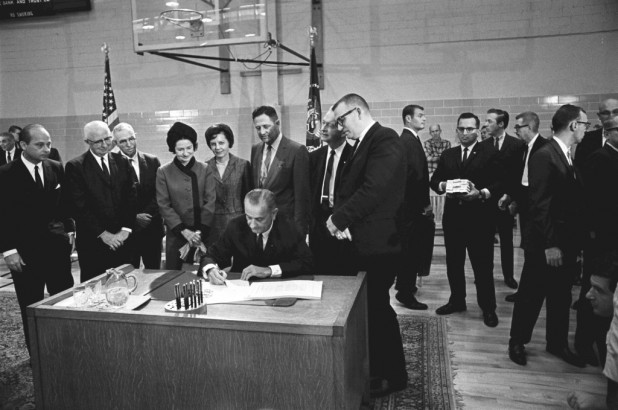

This is not the program that President Lyndon B. Johnson envisioned when he signed one of the signature bills of his Great Society program, the Higher Education Act of 1965.

Credit: Frank Wolfe/LBJ Presidential Library

A linchpin in Johnson’s effort to wipe out racial injustice and poverty, the act was meant to ensure that any student who wanted to go to college would be able to through federal scholarships and loans. “This nation could never rest,” Johnson stressed, “while the door to knowledge remained closed to any American.”

Before the law, most Americans who wanted to go to college had to finance it themselves. That meant paying out of their own pockets, securing a scholarship or taking out an expensive private loan. After the bill, students could go to a bank for a less costly student loan guaranteed by the federal government.

Under President Richard Nixon, Congress expanded the program in 1972 by creating a quasi-governmental agency – the Student Loan Marketing Association, or Sallie Mae – to increase the amount of money available for student loans.

Sallie Mae was viewed as an enlightened expansion of Johnson’s program because it established a market for federally backed student loans. Banks loaned to students, and Sallie Mae bought the loans from the banks, increasing the pool of money available for loans.

When the children of the Great Society had children of their own, the government’s role in student loans dramatically changed. President Bill Clinton would be the catalyst for change – but not in the way he wanted.

After he was elected in 1992, Clinton pushed through Congress a major revision of the student loan program that made the federal government the direct lender of the loans – not just the insurer.

Clinton’s program eliminated the middleman between the government-backed loans and students. The direct loan program alarmed Sallie Mae and the banks: Now they had to compete with a government-run program that could make loans at a lower interest rate without having to turn a profit.

When Republicans won control of Congress in 1994, they moved to kill the direct loan program and privatize Sallie Mae. A year of bitter political infighting ensued until Clinton and congressional Republicans reached a compromise, one that ostensibly saved his program. In return, Clinton agreed to privatize Sallie Mae.

Upon passage of the bill in 1996, Rep. Howard P. “Buck” McKeon, a California Republican, hailed privatization, saying it was “paving the way to the future of a smaller, less intrusive government.”

Clinton’s direct loan program had been saved, but it soon would be marginalized by Sallie Mae.

Before privatization, Sallie Mae had little flexibility: The U.S. president appointed one-third of its board, and the Departments of the Treasury and Education had to sign off on most major policy decisions. It couldn’t loan money to students; the banks did that.

The compromise freed Sallie Mae of those restrictions. Originally barred from acquiring other loan issuers, back-office operations or collection agencies, it now could buy any company. Earlier, it lacked the authority to issue federally guaranteed loans; now it could do so. And for the first time, Sallie Mae could make private student loans – ones not guaranteed by the federal government – that commanded much higher interest rates and greater profits.

Suddenly, a full array of services that had been parceled out among government agencies or contractors – from making loans to collecting premiums and penalty fees – could be consolidated under Sallie Mae’s umbrella.

Privatization had a dramatic impact. While the Department of Education technically still oversaw student loans, the message out of Congress couldn’t have been clearer: Bureaucrats, step aside and let the private market run the loan program.

Sallie Mae dominates the market

Credit: Susan Biddle/The Washington Post/Getty Images

The man who would make the most of this newly privatized industry was Albert Lord, who became CEO of Sallie Mae in 1997. Tall and lean, Lord looked like a patrician born to the manor, but he was the son of a newspaper linotype operator whose approachable nature masked his driving ambition.

Under Lord, Sallie Mae grew by leaps and bounds. Free of government control, it emerged as the dominant company in the field.

Lord’s chief competition when he took over was the Education Department’s direct loan program created by Clinton. Since its adoption in 1993, the program had gained popularity steadily on college campuses and captured a third of the student loan market by the time Sallie Mae was privatized.

Sallie Mae undermined the federal program with sheer marketing muscle. The company paid colleges to drop out of the federal program and make Sallie Mae the campus student loan provider. It paid college financial loan officers to serve as consultants on Sallie Mae advisory boards. It paid a New Jersey agency $15 million to steer business to Sallie Mae.

It placed Sallie Mae employees in university call centers to field questions from students who thought they were getting advice from college loan officers. It sponsored trips and cruises for collegiate financial aid officers. Other student loan lenders engaged in similar practices. Needless to say, the Department of Education didn’t have a budget to entertain college aid officials with free cruises on the Potomac River.

Faced with industry lobbying and congressional opposition, the Department of Education struggled to maintain Clinton’s direct loan program. After President George W. Bush took office in 2001, the program was cut back further. By 2007, its share of the student loan market haddeclined by more than 40 percent.

There’s no hard number for how much this will end up costing taxpayers. Projectionsfrom 1992 suggest the price tag will be billions of dollars.

Sallie Mae also began marketing private student loans. These loans have higher interest rates and fees and give borrowers fewer options for relief if they run into financial trouble.

Nevertheless, college loan officers say many students succumb to the sales pitch of private lenders because they either don’t realize that private loans are more expensive or have maxed out their federal loans. Private loans make up a small portion of the total student loan debt, but it’s still a huge number: about $100 billion.

Lord had created an integrated student loan operation encompassing every phase of the burgeoning industry. And the company became a financial juggernaut. In the decade after it was privatized, Sallie Mae’s stock price rose by 1,900 percent. From 1999 to 2004, Lord’s compensation topped $200 million. From 2010 to 2013, when students began to shoulder more and more debt, Sallie Mae’s profits were $3.5 billion.

Lord retired in 2013. The following year, Sallie Mae spun off most of its student loan business into a new company, Navient.

Lord declined to be interviewed for this story. In an email, he blamed the federal government and universities for the surge in student debt.

In the past 20 years, there has been “geometric growth in annual government student lending,” Lord said. This explosion in government lending has left taxpayers at risk for more than $1 trillion, he wrote, while allowing colleges to inflate the cost of higher education at the same rate that students rack up debt.

“The notion that private lenders … caused the monumental mortgaging of college graduate futures is a fantasy,” Lord wrote.

After privatization, Sallie Mae became a powerful political force in Washington. Since 1997, the company has spent more than $44 million lobbying Congress, the president and the U.S. Department of Education on hundreds of measures, according to the Center for Responsive Politics. Sallie Mae’s political action committee and company executives, led by Lord, have pumped about $6 million into the campaigns of favored politicians – half to Republicans, half to Democrats.

In Congress, the biggest recipient was Ohio Republican John Boehner.

Before he was elected speaker of the House in 2011, Boehner served as chairman of the Committee on Education and the Workforce, where Sallie Mae had frequent business. From 1995 until his retirement in 2015, Boehner and his Freedom Project PAC received $261,000 from Sallie Mae donors, records show.

Boehner flew with Lord on Sallie Mae’s corporate jet for golf outings in Florida, The Chronicle of Higher Education reported in 2006. Meanwhile, Boehner went out of his way to make it clear that he’d protect the industry.

In 2006, as Congress considered slashing federal money for the student loan program, Boehner gave a speech to the industry’s trade association reassuring its leaders that they would be protected from cuts.

“Know that I have all of you in my two trusted hands,” he said. “I’ve got enough rabbits up my sleeve to be able to get where we need to.”

Boehner declined to be interviewed for this story. A spokesman said his efforts on behalf of the private student loan industry reflected his support for free enterprise and skepticism about big government.

“The policy actions he took in the House had nothing to do with political donations or anyone lobbying him,” David Schnittger wrote in an email.

The states withdraw from funding higher education

Credit: Courtesy of Saul Newton

In the summer of 2010, Saul Newton was a 20-year-old rifleman stationed at a small U.S. Army outpost in the remote, dangerous Arghandab River valley of Afghanistan.

It was a radical change for a kid from suburban Milwaukee who only months before had been a communications major at the University of Wisconsin-Stevens Point.

But after two years of tuition hikes, Newton found himself with $10,000 in student loans and the prospect of still more borrowing if he stayed in school.

“I couldn’t afford it anymore,” he said. He dropped out and enlisted, hoping to go back to college one day under the GI Bill.

He wound up fighting the Taliban. His unit’s worst day was Aug. 30, 2010, when a roadside bomb killed the battalion chaplain and four other soldiers.

“My focus was on doing my job and staying alive,” Newton said. But no matter what else was going on at the outpost, he said that once a month, he made his way to the wooden shack where the unit kept a laptop with a satellite internet connection. There, he made an online student loan payment of $100.

It was crazy that a soldier in a war zone had to worry about his student loans, Newton said. But he believed that if he didn’t pay his loans, “my credit would be shot.” The government offers student loan deferments to troops in wartime, but Newton said no one told him that.

Today, back home as executive director of the Wisconsin Veterans Chamber of Commerce, Newton said his state’s cuts to higher education will force more young people to face the same choices he did: Borrow or enlist.

“You shouldn’t have to go to war to get a college education,” he said. Newton hasn’t gone back to school.

In the last decade, Wisconsin has cut back sharply on appropriations for its state university system.

In 1974, state support for higher education was $14.73 per $1,000 of personal income, according to an analysis in the Milwaukee Journal Sentinel. By 2013, Wisconsin had withdrawn nearly two-thirds of that support, to $5 per $1,000.

The cuts deepened after Republican Scott Walker was elected governor in 2010.

When Walker took office, students paid about 37 percent of the cost of their education, according to data compiled by the State Higher Education Executive Officers Association. By the end of Walker’s first term, it was 47 percent.

Amy Pyle – Editor in Chief @ Reveal from The Center for Investigative Reporting

Gwendolyn Bounds – Executive Director, Content @ Consumer Reports

Note: Joaquin Alvarado, CEO of The Center for Investigative Reporting, is on Consumer Reports’ board of directors.

By then, 70 percent of Wisconsin students graduated with debt – the third-highest percentage in the nation, according to the nonprofit Institute for College Access & Success.

Walker’s press office didn’t respond to repeated requests for comment. Walker froze tuition for in-state students in the University of Wisconsin System in 2013 but has continued to cut its budget byhundreds of millions of dollars. This month, he told Wisconsin Public Radio that he was considering providing extra support to the university.

Wisconsin’s trajectory follows a national trend.

After World War II, states appropriated more funds for public higher education and by 1975 were contributing 58 percent of the total cost. But since then, they have reduced their share steadily, pressured by, among other things, the rising costs of Medicaid and prisons. Today, it’s at 37 percent nationally, according to data from the U.S. Bureau of Economic Analysis.

To Thomas G. Mortenson, a senior scholar at The Pell Institute for the Study of Opportunity in Higher Education, the numbers reflect the betrayal of America’s youth.

“We ought to invest in the future, not take from the future,” said Mortenson, who has studied state funding trends for years. “Where I used to live, we called that eating our seed corn.”

Nearly every state pays a smaller percentage of the cost than in years past. A Chronicle of Higher Education study showed that in the quarter-century up to 2012, state support declined sharply. At the University of California at Santa Barbara, it plummeted from 54.1 to 23.4 percent. Michigan State University fell from 45 to 17.8 percent. At the University of Virginia, state support dropped from 36.9 to 14.4 percent.

As states cut back, universities raised tuition. To cover the increase, more students borrowed. It all meant more money for the loan industry.

Debt collection becomes a hot business

With a degree in criminal justice from La Salle University, a soaring loan balance and few prospects, Jessie Suren had begun to call herself “a student debt slave.” In 2012, she decided to work for the enemy, as she put it. Her job: collecting on delinquent student loans at a massive call center in Harrisburg, Pennsylvania.

For about $12 per hour, she was one of hundreds of telephone collectors jammed together in the vast boiler room-like office of American Education Services, a loan servicing concern and U.S. Department of Education contractor.

The work was automated and fast paced: Calls were robodialed, and the delinquent borrower’s account history flashed on the computer screen in Suren’s cubicle. Her job was to engage with the borrower, stick to the script and try to get some money.

Some calls were scary, Suren said: Angry debtors would curse and threaten her, declaring they were jobless and broke. Others were heartbreaking: Borrowers would claim they or their children were terminally ill.

Whatever the story, Suren said she’d have to tell them what would happen if they didn’t pay: The company would take their tax refund and garnish their wages.

After hanging up, Suren sometimes would reflect on her own student loans.

“This is going to be me in a couple of years,” she remembers thinking. After a year, she quit.

The federal government holds roughly 90 percent of the $1.3 trillion in outstanding student loans. That makes the Department of Education effectively one of the world’s largest banks, but one that rarely deals with its customers. That job has been turned over to private contractors that are paid commissions and sometimes bonuses to collect on student loans.

At first, federal employees in the Department of Education handled student loan collections, but starting in 1981, the department began contracting with private companies to take over some debt collection.

After Sallie Mae’s privatization in 1996, investors poured into this field. Private equity funds controlled by JPMorgan Chase & Co. and Citigroupbought established debt collection firms, as did a fund led by one of Mitt Romney’s former partners at Bain Capital. Some family-owned debt collectors, such as NCO Financial Systems, became hot properties and would be sold to one private equity fund after another.

Today, 1 in 4 borrowers are behind in their payments, with nearly 8 million in default.

As borrowers struggle to make their payments, student debt has become the go-go sector of the debt collection industry. Under Education Department contracts, the more collectors recoup, the more they earn. Contractors are expected to make more than $2 billion in commissions from the government this year.

With the stakes so high, complaints about overzealous debt collectors have soared. Federal and state agencies have fined contractors millions for misconduct in harassing student debtors. Some bad actors have lost their contracts entirely.

Credit: Peter van Agtmael/Magnum Photos

San Francisco graphic designer Brandon Hill said Sallie Mae collectors began calling him at 5 a.m. “yelling and screaming” about his past-due payments. After he complained to state regulators, the barrage of predawn calls stopped. But in 2014, Sallie Mae and Navient sued Hill for immediate payment of $73,000 in student loans, records show.

“I was sued for complaining,” he said. He’s negotiating a settlement.

In a letter to the state, Sallie Mae wrote that the company had “acted appropriately” in contacting Hill. The 5 a.m. calls occurred because Hill’s cellphone has a Virginia area code, so collectors assumed he was on the East Coast, a Sallie Mae official wrote.

Retired University of Cincinnati professor Mary Franklin said collectors threatened to seize her disability insurance benefits because she fell behind on a student loan for the first time in 20 years. She said the threats occurred after she became ill in 2002.

Credit: Peter van Agtmael/Magnum Photos

“I tried to explain to them that I was ill and I was still coming out of it,” she said. “They said the federal government (doesn’t) care.” She managed to resume payments.

Congress revised the student loan program in 2009 to take back control of issuing federal loans. However, it left intact the industry that had grown up to service and collect on the loans. The House Committee on Education and Labor went out of its way to stress in its report that “the legislation does not force private industry out of the system.”

In 2015, the Obama administration launched a pilot program to test whether federal employees could effectively take over the job of collecting on defaulted student loans, while being more helpful and less aggressive than private collectors.

To Deanne Loonin, who monitored student debt for years for the National Consumer Law Center, the Treasury Department experiment is focusing on one of the biggest problems borrowers confront.

“We need to eliminate the private collection agencies from this process,” she said. “They are incentivized just to collect money, not to work out ways that might be better for the borrowers. We need to see what else might work.”

Student debt becomes the worst kind of debt

Credit: Peter van Agtmael/Magnum Photos

This year, presidential candidates Hillary Clinton and Donald Trump are promising reforms. But most proposed fixes offer limited relief for the 42 million Americans already saddled with student loans, such as Anita Brewer.

Brewer wanted to be a fashion designer when she enrolled at the Los Angeles campus of American InterContinental University in 2005.

The school was hot. Its parent company, Career Education Corp., was beloved by Wall Street. In that era, investment firms saw huge potential for high profits and little risk in owning for-profit schools.

Their business model was simple: The more students they recruited who were eligible for a federal loan, the more money they made. Never mind that many students dropped out before earning a diploma and were left with debts they couldn’t repay.

Brewer had no idea that Career Education’s schools already were a magnet for complaints about poor academic quality, massive student turnover, high student debt and securities fraud.

The year she arrived, the trouble exploded into view. An accrediting agency put the school on probation. Then, in 2008, the company announced that it would close the L.A. campus. By that time, Brewer had taken out $60,000 in federal and private loans.

She tried to transfer, but other colleges refused to accept her credits. With no degree, she worked at a series of low-paying jobs as interest on her student loans ballooned. Before long, Sallie Mae was demanding $1,000 a month in payment, an amount nearly equal to her monthly earnings.

She applied to a federal program that forgives student loans when a college shuts down. But the U.S. Department of Education contended that Brewer didn’t qualify because technically, the school hadn’t shut down – it still had campuses in the South and overseas. Meanwhile, the balance on her loans has risen to $157,000, and some were in default.

“I worked so hard not to be in this situation right now,” she said. “I sacrificed so much to go to school and get an education. But I can’t get an apartment, I can’t get a cellphone, I can’t get a car, I can’t get anything because my credit is shot to hell.”

In an earlier time, Brewer might have gotten some relief by going to bankruptcy court. That’s where Americans seeking a second chance long have been able to get a reprieve from their crushing debt.

But the powerful student loan industry closed off that option in 2005, the year Brewer enrolled in college.

After a seven-year, $100 million lobbying campaign by financial interests, Congress overhauled bankruptcy laws to make debt relief tougher on all debtors. Over the years, the measure was the subject of intense debate, 24 congressional hearings and even a presidential veto.

SEE THE FACES OF THE STUDENT DEBT CRISIS

But a provision that was worth a fortune to Sallie Mae and other issuers of private student loans was slipped into the bill with no debate – and with bipartisan support.

At a 1999 hearing, then-Rep. Lindsey Graham, R-S.C., proposed barring debtors from discharging private student loans via bankruptcy, a transcript shows. Rep. John Conyers, D-Mich., who was leading Democrats’ opposition, said he had no objection. Graham’s amendment passed by a voice vote and eventually became part of the law.

Rep. Jerrold Nadler, D-N.Y., said the private student loan issue “wasn’t really on the radar screen” for opponents.

“In retrospect, it should have been part of the debate,” he said, “although there were ample other reasons to oppose that bill.”

The measure’s practical effect was to put student debtors in the same category as drunken drivers, fraudsters and deadbeat dads and moms seeking debt relief. From then on, it was easier to go bankrupt if you were a playboy who’d run up credit card bills living large in the Caribbean than if you were a former student who’d gotten sick or lost your job.

The law gave lenders tremendous leverage over student debtors, no matter how dire their circumstances, said Daniel Austin, a bankruptcy law professor at Northeastern University.

“It’s really awful what we’ve done,” he said.

While the bankruptcy measure was pending, Sallie Mae spent about $14 million lobbying Congress, according to data from the Center for Responsive Politics. The company made about $2.2 million in campaign donations during that period, $16,000 of them to Graham, Federal Election Commission records show. Graham’s office didn’t respond to a request for comment.

Over the next few years, bills were introduced in the House and Senate to overturn the bankruptcy exclusion.

In 2007, the newly elected Democratic majority presented the industry with a new threat.

A confidential planning document that surfaced in press accounts at the time shows Sallie Mae’s plan: Hire a public relations firm with ties to the Democrats. Meet with members of the Congressional Black and Hispanic caucuses to impress upon them how Sallie Mae was all about helping their low-income constituents. Set in motion grassroots efforts to turn back any action in Washington that might restrict Sallie Mae.

Later that year, Sen. Dick Durbin, an Illinois Democrat, introduced a bill to treat private student loans like any other debt in bankruptcy. It went nowhere, as have similar bills since.

The success was a testament to Sallie Mae’s evolution from a quasi-government agency into a full-fledged special interest in Washington whose primary goal is to protect and advance its own interests.

The government gets rich, too

The Department of Education has little incentive to fix the core problem. The loan program that began with the principal goal of helping disadvantaged students pay for tuition has become a moneymaker for the federal government.

The profit arises from the government’s ability to borrow money at a low rate and then lend it to students at a higher rate, thus charging students more than is necessary to recoup its costs.

The federal loans issued between 2007 and 2012 currently are projected to generate $66 billion in income for the government, according to a Government Accountability Office report.

Congress in 2013 lowered the interest rate on loans for incoming student borrowers, yet refused to extend the same benefit to more than 40 million student loan holders who had borrowed previously.

Credit: Bill Clark/AP Images/CQ Roll Call

At a Senate hearing in 2014, Sen. Elizabeth Warren, the Massachusetts Democrat, quizzed the head of the Federal Student Aid office, James W. Runcie, about the government’s loan income.

Warren: “My question is … where do those profits go? Do they get refunded back to the students, who paid more than was necessary for the cost of their loans? Or are they just used to fund government generally?”

Runcie: “They are used to fund government generally. They do not come back specifically into the program.”

Warren: “We’re charging more interest than we need to run the student loan program, and there’s no mechanism to refund that money to the students. … I don’t think the student loan program should be designed so that it’s making profits for the federal government.”

But this is the way it works, and it’s another example of how government policy continues to harm millions of students.

If you are old or partially disabled or both – and have an outstanding student debt, even one going back decades – the government still can take a portion of your Social Security check. Or your parents’.

Richard Brown, 65, of Ossining, New York, knows about that.

In 2004, Brown and his wife had good jobs in information technology. He took out $50,000 in federally guaranteed student loans for his daughter because he didn’t want her to go into debt, and they could afford to help her.

But then the recession hit. Brown lost his job in 2009 and at 58 couldn’t find another. Three years later, his wife lost her job when her company was acquired by a competitor. Their debts mounted, and by 2013, the student loans, because of compounding interest and penalties, had risen to $135,000.

The couple filed for bankruptcy, but the student loans weren’t eligible. Brown was shocked when the federal government began taking $250 a month from his Social Security check of $1,700.

“This is money we need to live on,” he said. “To us, it’s a lot of money. We worked 35 or 40 years to be eligible. I had no idea they could do that.”

Not only can the government do that, but it’s doing so more often. The government can take as much as 15 percent of a debtor’s Social Security and in 2013 garnished benefits of 155,000 Americans who were in default on their federal student loans, according to a GAO report. That’s a fivefold increase in a decade.

By law, banks and credit card companies cannot seize Social Security benefits to collect debts. But in 1986, Congress gave the U.S. Treasury the go-ahead to garnish Social Security payments to collect money owed to the government.

The amount of money the government has raised by garnishing Social Security benefits – $150 million in 2013, for example – is a tiny fraction of the $1.2 trillion that borrowers owe the government for federal student loans.

After the federal government garnished Brown’s Social Security, he and his wife lost their cooperative apartment to foreclosure. They moved in with their daughter.

As for the student loan industry, it keeps rolling along.

Look no further than the handsome I. M. Pei-designed building in downtown Wilmington, Delaware, where a student loan startup is making waves.

College Ave Student Loans bills itself as “the leading next-generation student loan marketplace lender.” With claims that it will disrupt the multibillion-dollar student loan industry, College Ave has said it is going to bring “innovation to a long-stagnant market.”

Behind those claims are some familiar faces.

Two former Sallie Mae executives founded the company in 2014. It’s had no trouble raising $40 million from venture capitalists and hedge fund investors.

There’s one other investor in College Ave who knows a lot about making money in the student loan industry: Albert Lord.