Above Photo: Dave Dugdale/Flickr

In recent weeks, a number of policy analyses of progressive economic policies—a surtax on high-incomes, a wealth tax, and Social Security expansion—have claimed these policies would damage economic growth. Policymakers should give these analyses very little weight in debates about these issues, for a number of reasons.

First, and most important, is the fact that all of these analyses are grounded in an economic view of the world that sees growth as constrained by the economy’s productive capacity (or the supply side of the economy) and not by the spending of households, businesses and government (the economy’s demand side). These estimates have other problems too—they are not even particularly convincing supply-side estimates and even if the economy’s growth really was constrained by supply, these estimates would still be misleading about the effects of these policies on welfare. But the biggest reason why policymakers should give these analyses zero weight is because they assume that growth is almost never demand-constrained.

Before the Great Recession, the assumption that growth was nearly always supply constrained was almost universally held by economists and macroeconomic policymakers. It was recognized that demand (or aggregate spending) could occasionally be too weak to fully employ the economy’s productive capacity and hence cause rising unemployment, but it was generally thought that such periods were rare and would end quickly after the Federal Reserve sensibly cut interest rates. Because shortfalls of demand relative to supply were rare and short and easy to fix, the reasoning went, any real constraint on the economy’s growth over the long-run must be the pace of growth of supply. Growth in supply is generally driven by growth in the quality of the workforce, the productive stock of plants, equipment and research, and growth in technological progress, which together lead to growing productivity—or the amount of income or output generated in an average hour of work.

The assumption that supply constraints are much more likely to bind overall growth than demand constraints drove almost all macroeconomic policymaking in the decades before the Great Recession. For example, the Federal Reserve for decades feared lower unemployment far more than lower inflation. Lower unemployment was a signal that demand was rising relative to supply, and if one thinks growth was generally supply-constrained, this meant that demand growth would quickly outstrip supply growth and lead to rising inflation. Lower inflation, conversely, meant that supply growth was outpacing demand growth—but that was always a temporary and easy-to-fix condition. The decades-long bipartisan overreaction to rising federal budget deficits is also a byproduct of assuming the economy’s growth is supply constrained. Deficits boost demand growth. If one assumes that demand is generally marching in lock-step with supply, then larger deficits that boost demand imply that supply constraints will soon bind and cause inflation (or interest rate increases). Smaller deficits, conversely, reduce demand growth. But if the danger of demand growth slowing too much is low and easy-to-fix, then that’s not a problem.

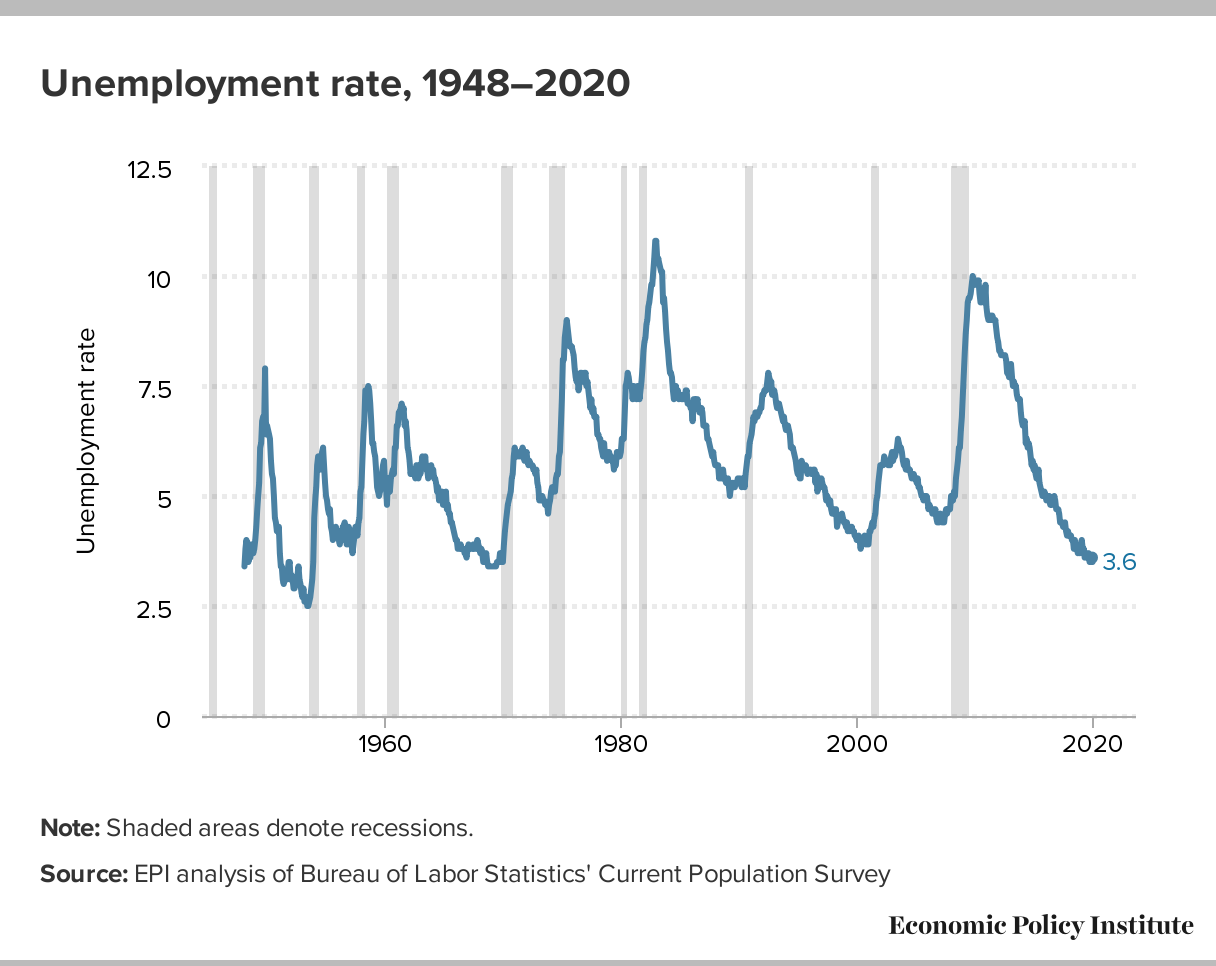

The experience of the last decade has done much to shake this belief that demand-constrained growth is nothing to worry about and that supply-constrained growth should be the default presumption for policy analysis. For example, the Federal Reserve has cut interest rates to spur demand growth three times in the past six months with unemployment below 3.8 percent. They certainly seem to be acting (correctly) as if demand-constrained growth is a real problem. Prominent macroeconomists and former policymakers like Olivier Blanchard, Jason Furman, and Lawrence Summers have all written in recent months that efforts to close budget deficits should not be a high policy priority, largely because there is no evidence that supply constraints are binding. These reversals of policy presumption are evidence-based and admirable. Yet the decades-long inertia of policy evaluation done in a framework of supply-constrained growth is hard to stop—and so we have the recent parade of analyses claiming that a number of progressive initiatives will slow the economy by dragging on supply side growth.

The Tax Foundation, for example, has estimated that a ten percentage point surcharge on incomes over $2 million—a change that would only affect the highest-income 0.1 percent of households—will slow growth enough to cost 118,000 jobs by the end of the decade. A still-preliminary analysis of presidential candidate Elizabeth Warren’s wealth tax—a change that would affect only the wealthiest 0.1 percent of households—was estimated by the Penn-Wharton Budget Model team to slow growth by more than 0.2 percentage points each year over the next decade. The Penn-Wharton Budget Model project’s assessment of a plan by Representative John Larson (D-Conn. ) to expand Social Security benefits was analyzed by my colleague Monique Morrissey previously, so I will largely leave that aside in this post.

Each of these results is driven entirely by the assumption that growth is supply-constrained. In the case of both the high-income surcharge and the wealth tax, the taxes are assumed to reduce labor supply and savings (which raises the “user cost of capital” and hence leads to reduced investment).

But over the past decade, there is no evidence that labor supply has been a constraint on growth. Unemployment rates fell steadily in the years between 2010 and 2018. Even as the decline in unemployment moderated over the past year, labor force participation rose smartly. Additionally, the share of prime-age adults with jobs remains below its 2000 level—and there’s no particular reason to be sure that 2000 level is a hard upper bound. The clearest sign that availability of labor has become a supply-side constraint would be rapid wage growth— and that has certainly not happened.

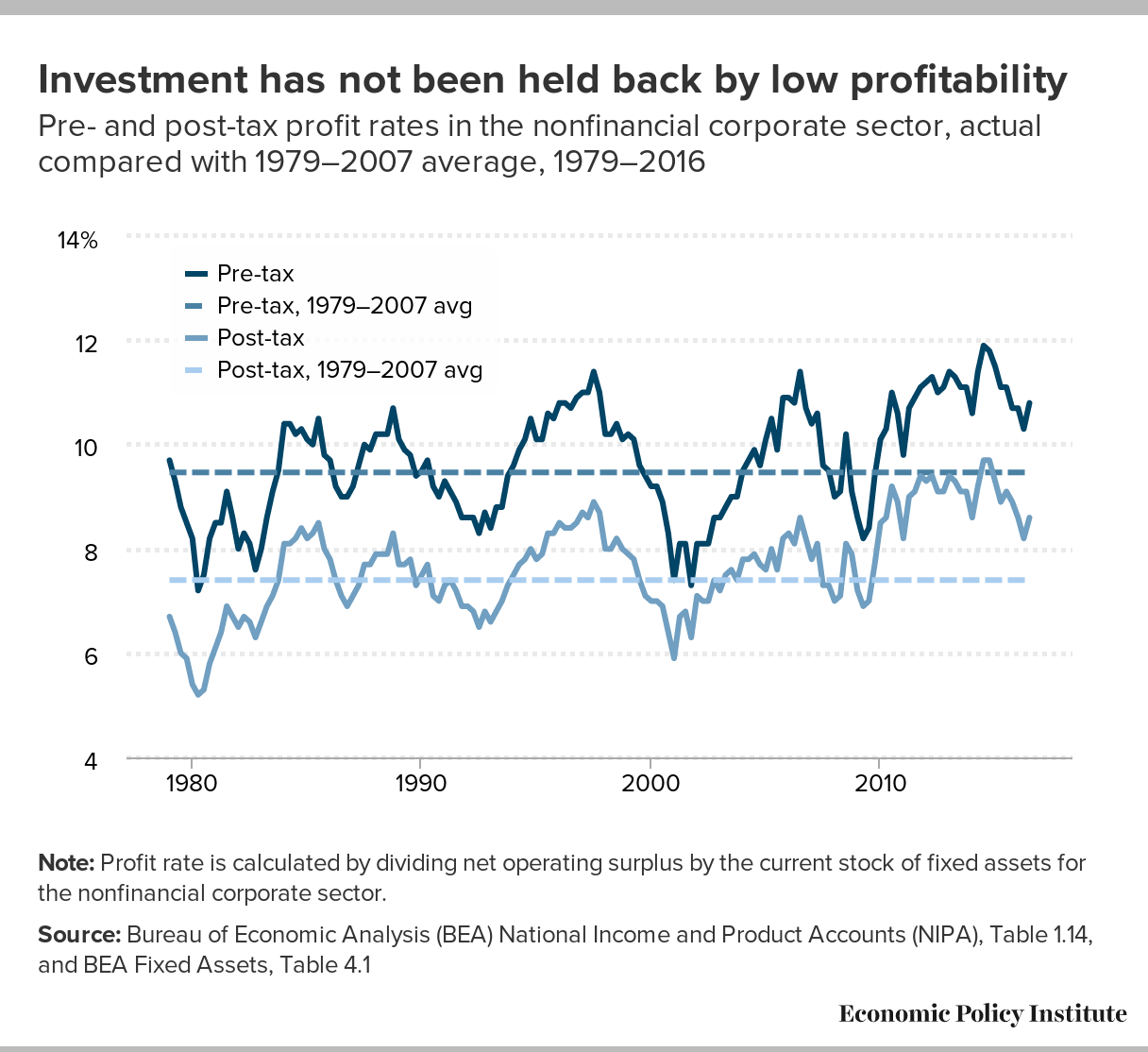

There is even less evidence that insufficient savings or a high user cost of capital have been constraints on growth of the capital stock or will become constraints anytime soon. Interest rates—the simplest proxy for the scarcity of savings and high user costs of capital – have been severely depressed for years, and interest rate projections have overestimated their growth since the late 1990s. Corporate profitability has been extraordinarily high over the 2000s, even as investment has been weak.

One rebuttal to the argument that we should severely discount policy analyses based on supply-constrained assumptions is that we can’t bank on too-low demand being the primary constraint on growth forever. This is true—but hardly dispositive. The norm of conducting long-run policy analysis premised on the assumption that supply is the primary constraint on growth was never grounded in thinking that demand never constrained growth. Instead, it was assumed that while demand could bind, it would only do so for very limited times so could be largely ignored in the long-run. But, we just emerged from a period where demand unambiguously constrained growth for a decade—an entire budget forecasting window!

Worse, we know some of the primary reasons why demand has become a tighter and tighter constraint on growth over time. One of the most important is the rise in income inequality that has characterized recent decades. All else equal, a redistribution of income from low and moderate-income households to richer households will drag on demand growth, as richer households spend a smaller share of their income. There are potential policy offsets to this demand drag stemming from redistribution—most notably lower interest rates. But interest rates have been extraordinarily low over the last decade even as demand sagged. For a host of reasons, the strategy of fighting the demand drag of the enormous upward redistribution of income with lower interest rates seems to have lost any juice it may have ever had. Until there has been a reversal of this upward redistribution, it seems odd to think we should simply re-adopt the assumption that demand will stop being the primary constraint on growth.

Another rebuttal to the argument that it is demand and not supply that will be the more likely constraint on growth in coming years is that productivity growth in the U.S. economy has been extremely slow of late. With slow productivity growth, even historically sluggish demand growth can exceed growth in the economy’s productive capacity and cause the supply-side to bind much more often. But the productivity slowdown is itself likely a function of slack demand over the past decade. Workers and capital have been so cheap and so plentiful for businesses to hire over the past decade that incentives to squeeze more from each unit of labor or capital have been severely blunted. Tellingly, as labor became scarcer in recent years, productivity growth has begun to firm up. Granted, productivity won’t rise without bound if demand accelerates, but the larger point is that one cannot infer from the past decade of data that low productivity growth is a permanent condition that guarantees supply constraints will bind going forward.

Ironically, the three proposals recently dinged by supply-side analyses as slowing growth are all aimed at pushing back against the trend of rising inequality. As such, if adopted they would actually make it more likely that such supply-side analyses could be useful sometime in the future.

To be very clear about this, a world in which it is supply constraints that bind is better in many ways. Involuntary unemployment would no longer be a problem and both productivity and wages would be pushed up. But even in a supply-constrained world, the recent analyses of the high-income surcharge and the wealth tax would be deeply misleading in terms of their effect on Americans’ welfare. Take the simplest case of this: the decline in GDP and jobs allegedly caused by the high-income surcharge. The first thing to note is how completely trivial even the Tax Foundation’s estimated effects are: growth that is slower by 0.01 percent for the next decade, with cumulative losses reaching 0.1 percent by the end of that time. One way to think about this is to compare how long it would take us with the surtax to reach the level of GDP projected for December 31, 2029 without the surtax. The answer is that we’d hit this same no-surtax level of GDP a week or two later. Would anybody notice this? In the second quarter of 2019, estimates of GDP growth were revised down by 0.1 percent—a one-quarter revision as large as the 10-year impact estimated by the Tax Foundation for the surcharge. Did anybody notice this 2nd quarter GDP revision in their lived economic experience or actually feel poorer?

In regards to the job impacts, they are roughly equivalent to 900 fewer jobs per month created over the next decade. But the statistical standard error on the estimate of the number of jobs created each month by the Bureau of Labor Statistics is just under 70,000. Again, this is not a change anybody would notice. Even more importantly for assessing the welfare impact of these estimates, none of this job loss (assuming it happened and was noticed) would be involuntary—that is, willing potential workers who were unable to find a job because of the tax. Instead, the job loss would occur because a miniscule decline in productivity growth caused by reduced capital investment would reduce wages (by something on the order of 0.01 percent each year on average). Due to these lower wages (lower relative to a forecast baseline, mind you, not lower wages than today), potential workers would voluntarily decide to not work. Think of how little we should worry about these welfare effects: a worker who chooses to work when wages are $20 an hour, but chooses not to work when wages are $19.99 an hour was clearly on the knife-edge of this decision anyhow, with work providing very little extra utility relative to not working.

Or take the case of the wealth tax. The GDP losses chalked up to its effects come about because a decline in the after-tax return to holding wealth reduces the incentive of households to save and hence pushes up the “user cost of capital”, which in turn reduces investment and productivity growth. But households’ after-tax return to holding wealth is but one in a long list of inputs into the user cost of capital, and even the overall user cost of capital has been shown in empirical studies to have only weak effects on investment. To get a sense of how unconvincing model-based estimates of the effect of tax-based changes in the user cost of capital on investment are, note that the Penn Wharton Business Model (PWBM) actually predicted pro-growth effects from the 2017 tax cut—even though it was deficit-financed, which suppresses growth in their supply-side driven model (all else equal). The logic for how the 2017 tax law spurred growth in their model (even as it boosted deficits) was again through the channel of lowering the user cost of capital and spurring investment. And yet in the real world, capital investment collapsed shortly after the law’s passage. Outside of highly stylized and opaque models, efforts to empirically estimate the effect of taxes on capital income on investment come to mixed results.

Finally, as many have pointed out, the effect of tax increases on growth depends on what you do with the money collected. If the worry is that tax increases might reduce private-sector investment, one can allay that by using the revenue to finance public investments. Research suggests that because U.S. governments (both federal and sub-national) have been so stingy with public investments in the recent past that the rates of return to boosting these could be potentially higher than for private investments. This seems especially true in regard to investments that reduce the growth of greenhouse gas emissions or provide high-quality early education for kids. Tax increases that help finance a larger public role in providing health insurance which then bends the long-run cost curve of health care by squeezing out inefficiencies and rents from the American health system would also have strong effects in boosting American living standards—yet this is obviously not any part of the PWBM estimates.

Is any of this a call for economic nihilism—simply rejecting any finding that progressive policies may have effects we’d want to consider when debating them? Not at all. For example, the Earned Income Tax Credit (EITC) is a very popular policy among progressive policymakers. Yet high-quality research indicates that some of its benefits may leak away from low-wage workers and to their employers. Knowing this, pairing the EITC increase with a minimum wage increase can help ensure that more of its gains are captured by workers. Analogously, it is conceivable (but by no means assured) that the wealth tax could indeed reduce savings by the very wealthy. If direct empirical estimates confirmed that, this would be valuable information. If further research indicated that reduced national savings overall were a binding supply-side constraint on growth (unlikely in the near-term or medium-term) then researchers could next look at whether or not the wealth tax boosted savings by the non-wealthy (it might). If the net effect of the wealth tax showed that it reduced national savings and caused supply-side constraints to bind, then complementary policies could be considered. For example, some have put forward plans for universal Guaranteed Retirement Accounts, financed by a combination of broad-based tax increases and mandatory contributions from employers and employees. Such plans would increase national savings.

Genuine information about economic policies is good and useful. But the highly stylized output of models that assume supply-constraints on growth are the norm, and which are presented as effects on “growth” and “jobs” with no further context are notably unuseful, and often actively misleading in today’s policy debates.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}